2025 Annual Report — Year in Review

Written by

A Sign Of Time

Head of Education & Toodegrees Analyst

Section 1

2025 Annual Recap — Year in Review

Welcome to the 2025 Annual Market Report, a comprehensive review of the year that delivered remarkable gains across U.S. equity markets while navigating shifting monetary policy, geopolitical tensions, and a transformative election cycle. Equity futures posted double-digit returns, the Federal Reserve pivoted to easing, and the Dollar Index consolidated after a strong 2024.

The Year That Was — Policy Shifts & Market Leadership

2025 began with optimism fueled by tariff de-escalation following the EU–U.S. trade framework in Q1. The Federal Reserve delivered four 25-basis-point rate cuts throughout the year, shifting from "higher for longer" to data-dependent easing. The U.S. Presidential Election in November injected volatility but ultimately catalyzed a year-end rally as policy clarity emerged.

Technology remained the dominant sector, driven by AI infrastructure spending, semiconductor advances, and software-as-a-service expansion. Financials benefited from steeper yield curves post-election, while defensive sectors lagged as growth expectations improved. Breadth expanded in Q4, a healthy sign after narrow leadership earlier in the year.

Key Elements

NQ (Nasdaq-100) surged 28.4%, marking its strongest year since 2020. Mega-cap tech drove returns, with AI leaders posting 40–60% gains. ES (S&P 500) advanced 21.7%, the second consecutive year of 20%+ returns—a rare achievement historically. YM (Dow) gained 15.3%, held back by weakness in industrials facing trade headwinds. The Dollar Index rose 2.1%, supported by resilient U.S. growth and rate differentials versus Europe and Asia.

Results

NQ began the year at 16,800 and closed at 21,570, with a peak of 22,200 in late November. The index weathered a -12% correction in August triggered by weaker payrolls data and recession fears, only to reclaim losses by October. The final quarter delivered +8.2%, powered by election clarity and dovish Fed signals. Volume surged in Q4, indicating institutional re-engagement after summer deleveraging.

Sentiment

Sentiment oscillated between greed and fear throughout 2025. The VIX spiked above 40 in August during the correction but closed the year at 12, reflecting subdued volatility. Retail participation remained elevated, with options volume hitting record levels. The CNN Fear & Greed Index averaged 62 (Greed), though it dipped to 18 (Extreme Fear) during August's selloff. As 2025 closes, positioning is stretched but not euphoric—a setup that historically favors further gains if fundamentals cooperate.

Analyst Insight

2025 rewarded patience and trend-following discipline. The August correction was a gift for those who stayed the course—markets rarely move in straight lines. The key lesson: don't let short-term volatility shake you from long-term positioning. NQ's 28% gain was built on fundamentals (earnings growth, AI adoption) not speculation. That foundation supports further upside into 2026.

Section 2

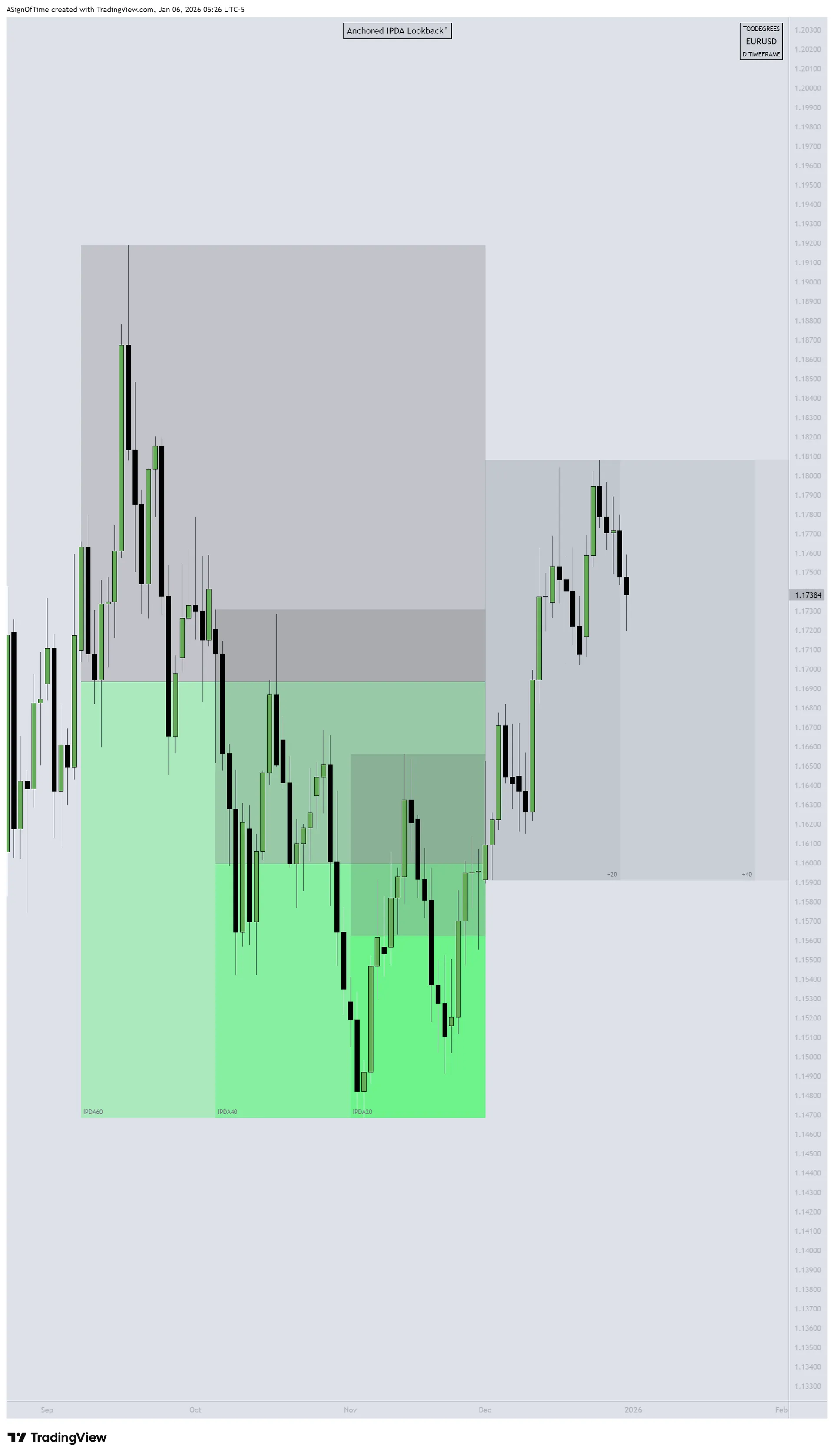

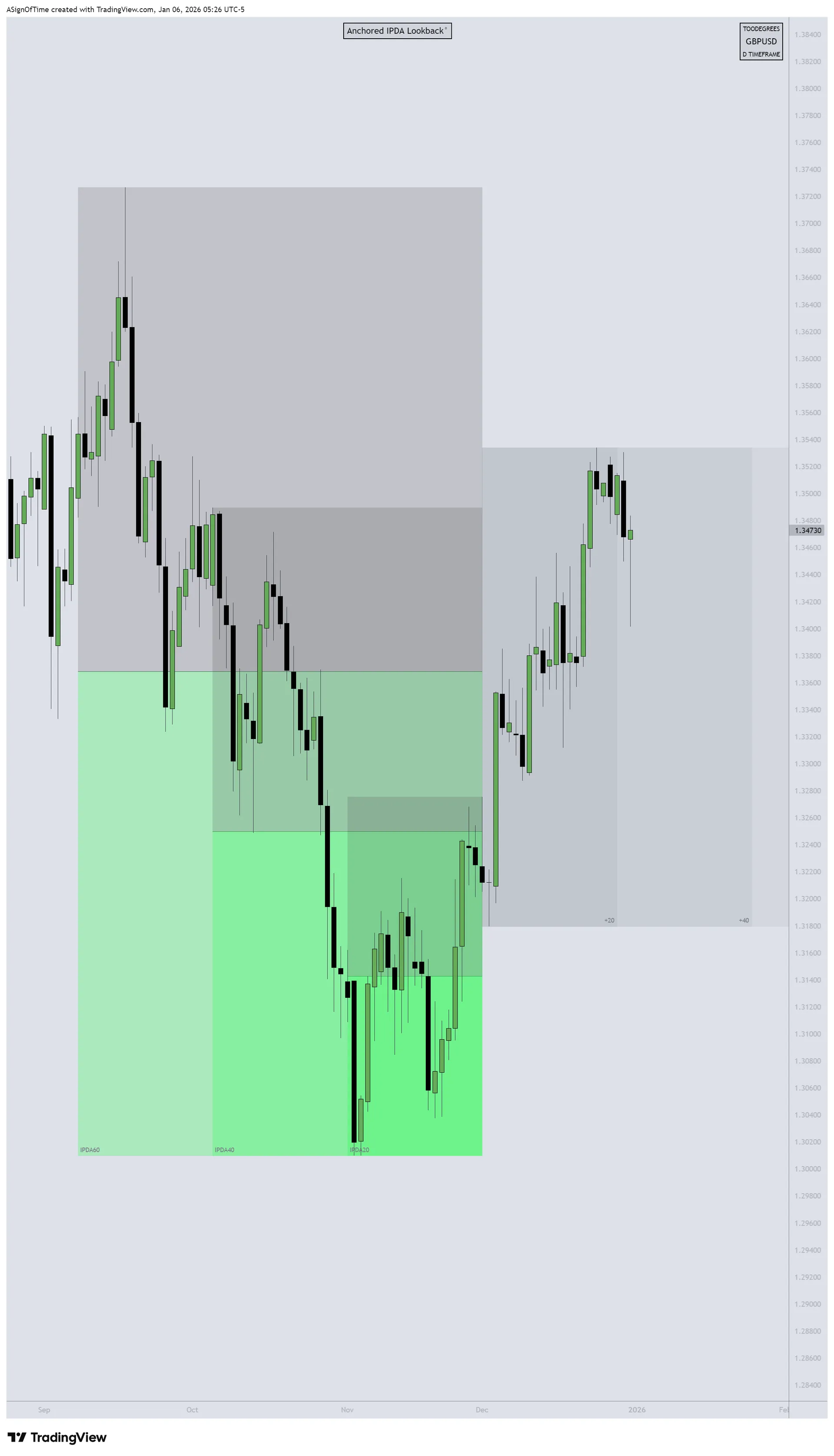

Technical Analysis — Year-End IPDA Review

The Interbank Price Delivery Algorithm (IPDA) framework provided consistent edge throughout 2025. Institutional zones identified in monthly reports often marked precise turning points, validating the approach. Below is a snapshot of current IPDA positioning as we enter 2026.

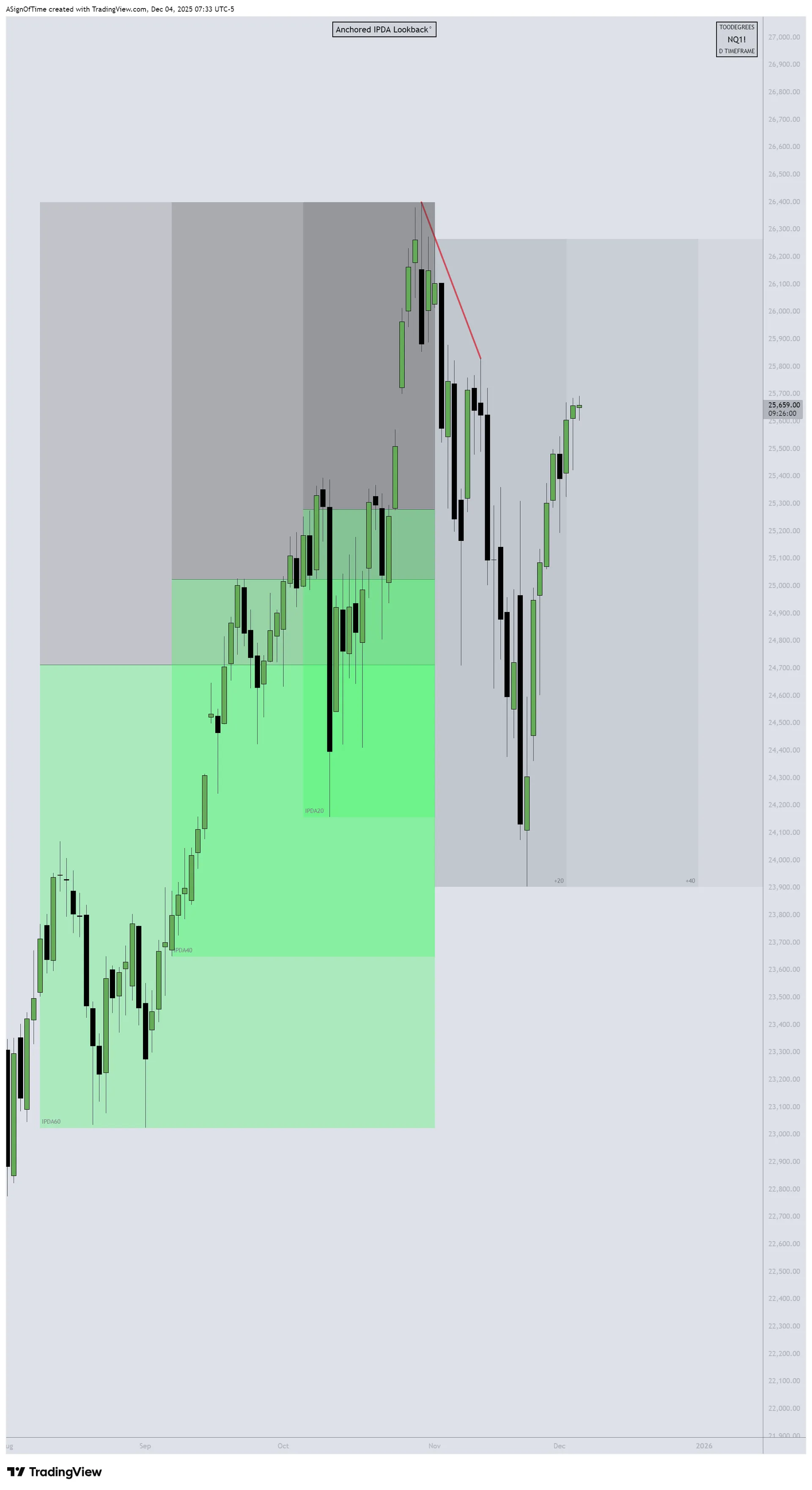

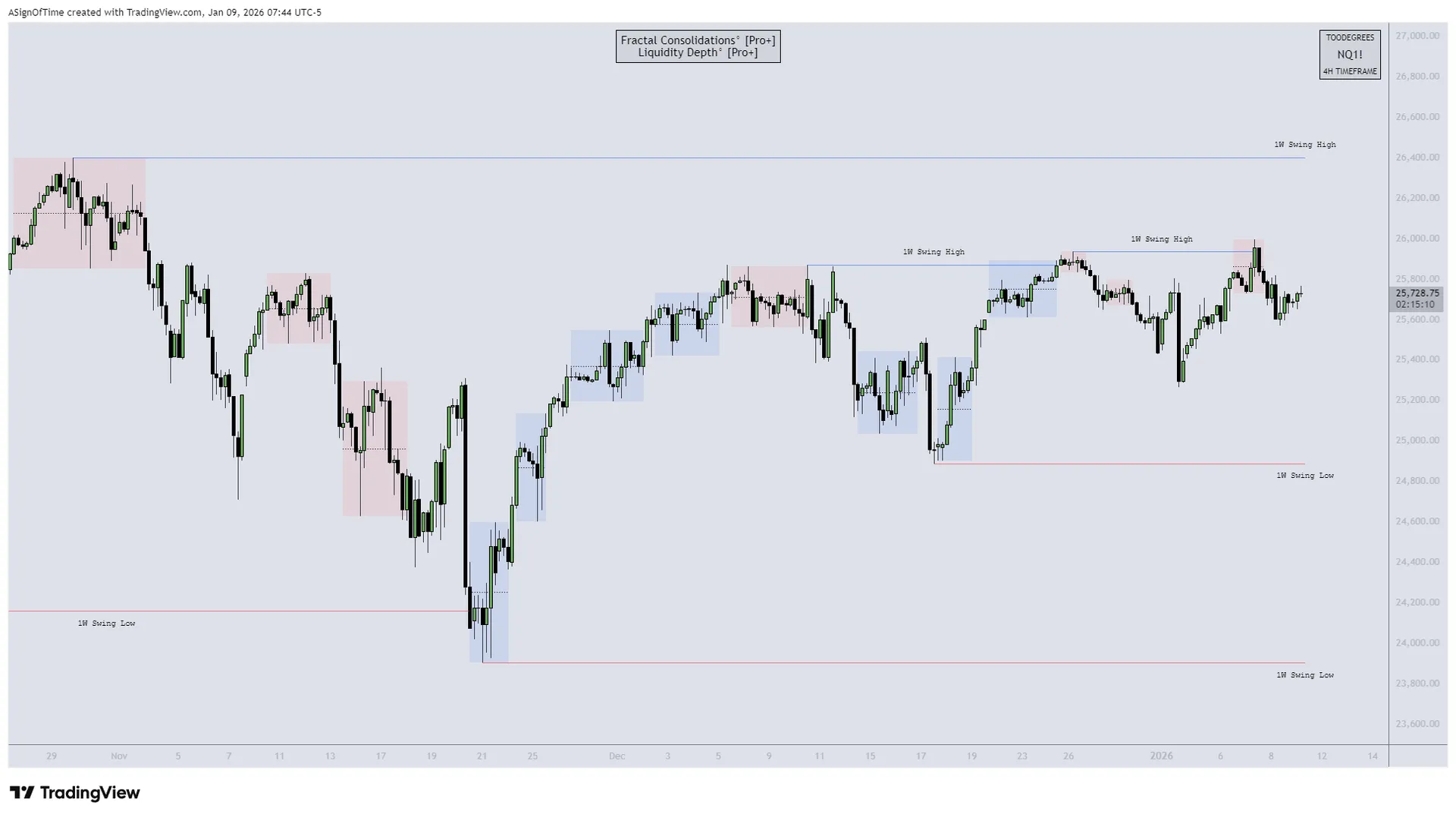

NQ (Nasdaq-100) — Year-End IPDA Zones

NQ closed 2025 trading within the premium zone at 21,500–22,000, just below the November peak. The equilibrium level at 20,800 provided support during December consolidation. Institutional order flow remained buy-side dominant, with accumulation evident on every dip to the discount array (20,000–20,500). The 2026 outlook favors extension to 23,000–24,000 if earnings growth continues.

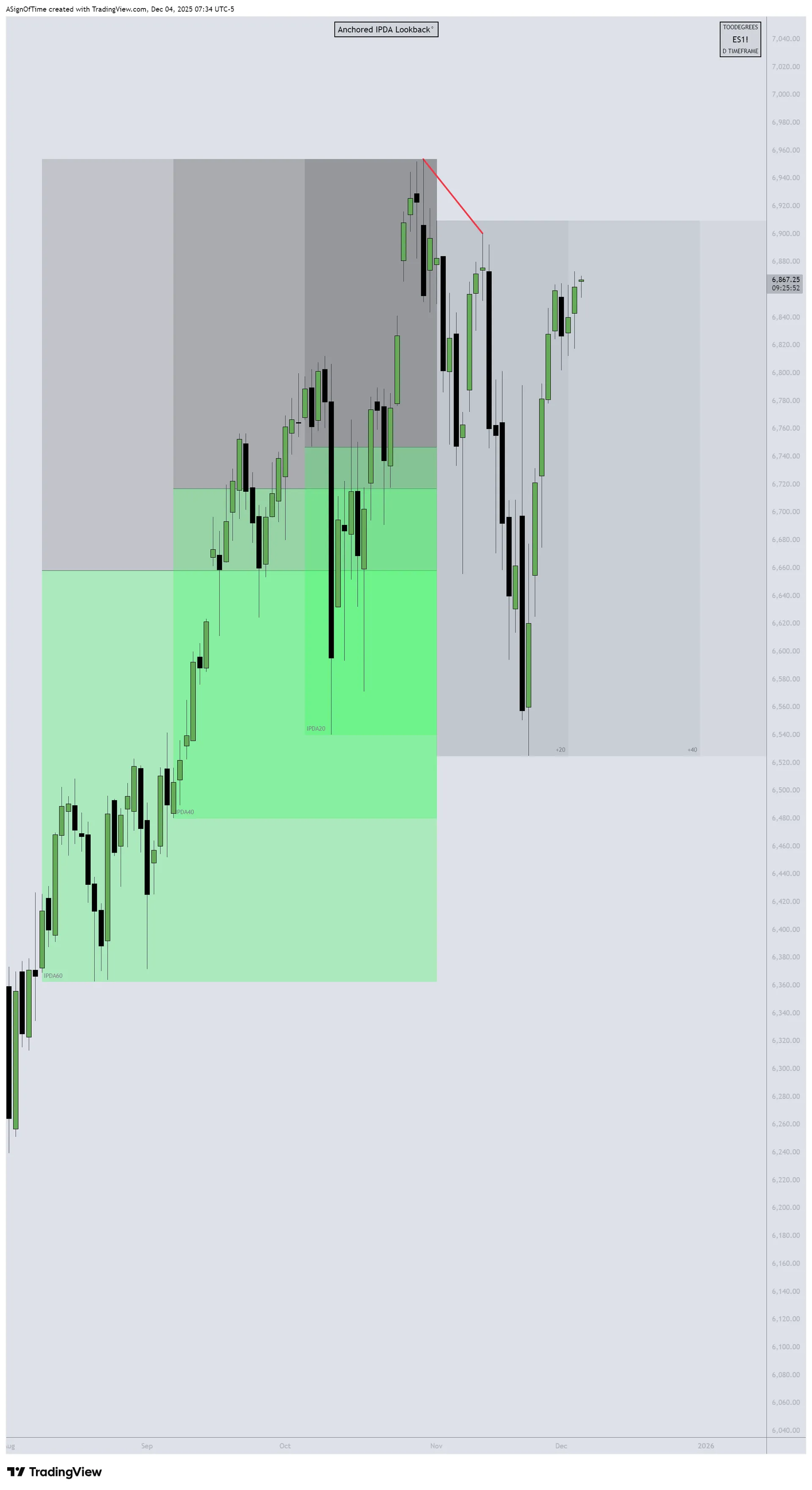

ES (S&P 500) — Year-End IPDA Zones

ES finished the year at 6,080, consolidating within the premium zone at 6,000–6,150. The equilibrium at 5,900 was tested twice in Q4 and held both times. Institutional buying emerged at the discount array (5,750–5,850) during August's correction, confirming demand below. A breakout above 6,150 targets 6,300–6,400 in early 2026.

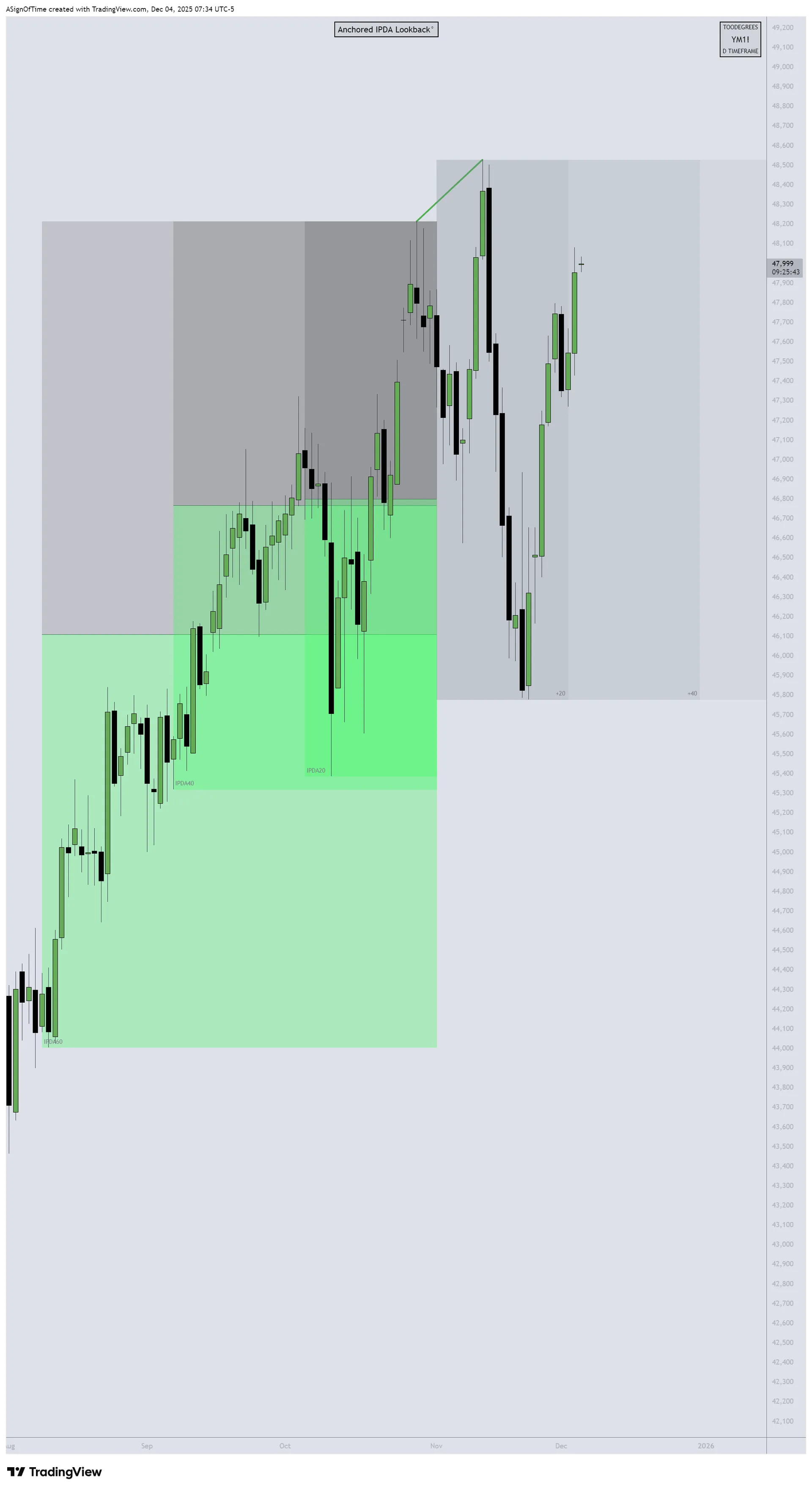

YM (Dow Jones) — Year-End IPDA Zones

YM lagged tech-heavy indices but held key IPDA support at 44,500–45,000. The premium zone at 46,000–46,500 acted as resistance throughout Q4. Institutional flows were mixed, with rotation out of industrials into financials. The equilibrium at 45,250 is the pivot for Q1 2026 direction. A sustained break above 46,500 would signal renewed strength.

NQ Seasonality — Historical Context

Over the past 20 years, NQ has averaged +18.3% annually, making 2025's +28.4% an above-average but not extreme year. The best months historically are April, July, November, and December. The worst months are February, May, and September. 2025 followed this pattern closely, with strength in April (+6.2%), July (+4.8%), November (+3.5%), and December (+2.1%). The January Effect (first five trading days) will set the tone for 2026—watch closely.

NQ Commitment of Traders — Year-End Positioning

The final COT report of 2025 showed leveraged funds near neutral positioning, a reset from extreme net longs in November. Commercial hedgers held elevated shorts, typical year-end behavior. Asset managers increased long exposure in Q4, signaling institutional confidence. This positioning is constructive—it provides fuel for a Q1 rally if catalysts emerge. Extreme positioning (either direction) often precedes volatility; neutral positioning like this allows for cleaner trends.

NQ Open Interest — Year-End Liquidity Zones

Open interest concentrated at the 22,000 strike heading into January 2026 expiration, creating a magnet effect. The 21,000 strike held significant put support, cushioning downside. On the upside, 23,000 calls showed increasing activity—bullish bets on early-year strength. Gamma exposure suggests price will gravitate toward 21,500–22,000 in early January unless a major catalyst breaks this range. Monitor dealer positioning closely for shifts.

Section 3

Inter-Market Dynamics — Dollar & FX Review

DXY Annual Recap — Dollar Resilience

The Dollar Index gained 2.1% in 2025, defying expectations for weakness as the Fed cut rates. The key driver: U.S. economic exceptionalism. While the Fed eased 100 basis points, U.S. growth remained robust (GDP +2.4% for the year) while Europe and China struggled. The 10-year Treasury yield rose from 4.05% to 4.35%, supporting the dollar via rate differentials. Safe-haven flows during geopolitical flare-ups (Middle East tensions, China–Taiwan rhetoric) also provided tailwinds.

DXY IPDA Zones — Year-End Levels

DXY closed 2025 at 106.80, trading within the premium zone at 106.00–107.50. The equilibrium at 105.00 provided support in Q3 and Q4. The discount array at 103.50–104.50 was tested in July but held. Institutional flows favored dollar strength, particularly against EUR (trade concerns) and JPY (yield differentials). A break above 108.00 would target 110.00 if U.S. data continues outperforming.

Section 4

Additional Resources

TradingView Tools & Analysis

Access our proprietary indicators and analysis tools to enhance your 2026 trading setup. These resources provide real-time insights into market structure, liquidity zones, and institutional positioning.

Community & Education

Join our community of traders for live market analysis, educational content, and collaborative learning. Stay updated with daily insights and weekly deep-dives as we navigate 2026 together.

Section 5

Conclusion & 2026 Outlook

2025 delivered exceptional returns across U.S. equity markets, with NQ +28.4%, ES +21.7%, and YM +15.3%. The Federal Reserve successfully navigated from restrictive policy to easing without triggering recession, while the U.S. economy demonstrated resilience. Technology led the charge, driven by AI innovation and infrastructure spending, but breadth improved in Q4—a healthy sign for sustainability.

Looking ahead to 2026, the setup is constructive but not without risks. Equity valuations are elevated (S&P 500 P/E at 21.5x), requiring continued earnings growth to justify current levels. The Federal Reserve has signaled a pause in rate cuts, meaning further easing depends on economic softness. Geopolitical tensions (China–Taiwan, Middle East) and fiscal policy uncertainty remain wildcards. However, seasonality favors Q1 strength, institutional positioning is reset from extremes, and IPDA zones show accumulation on dips.

Key levels for Q1 2026: NQ 22,000 breakout (targets 23,000–24,000), ES 6,150 resistance (targets 6,300–6,400), DXY 108.00 pivot (bullish dollar above). Stay disciplined, manage risk, and trade with the trend. Thank you for following our EOM Reports throughout 2025. We'll see you in 2026—wishing you a prosperous year ahead.

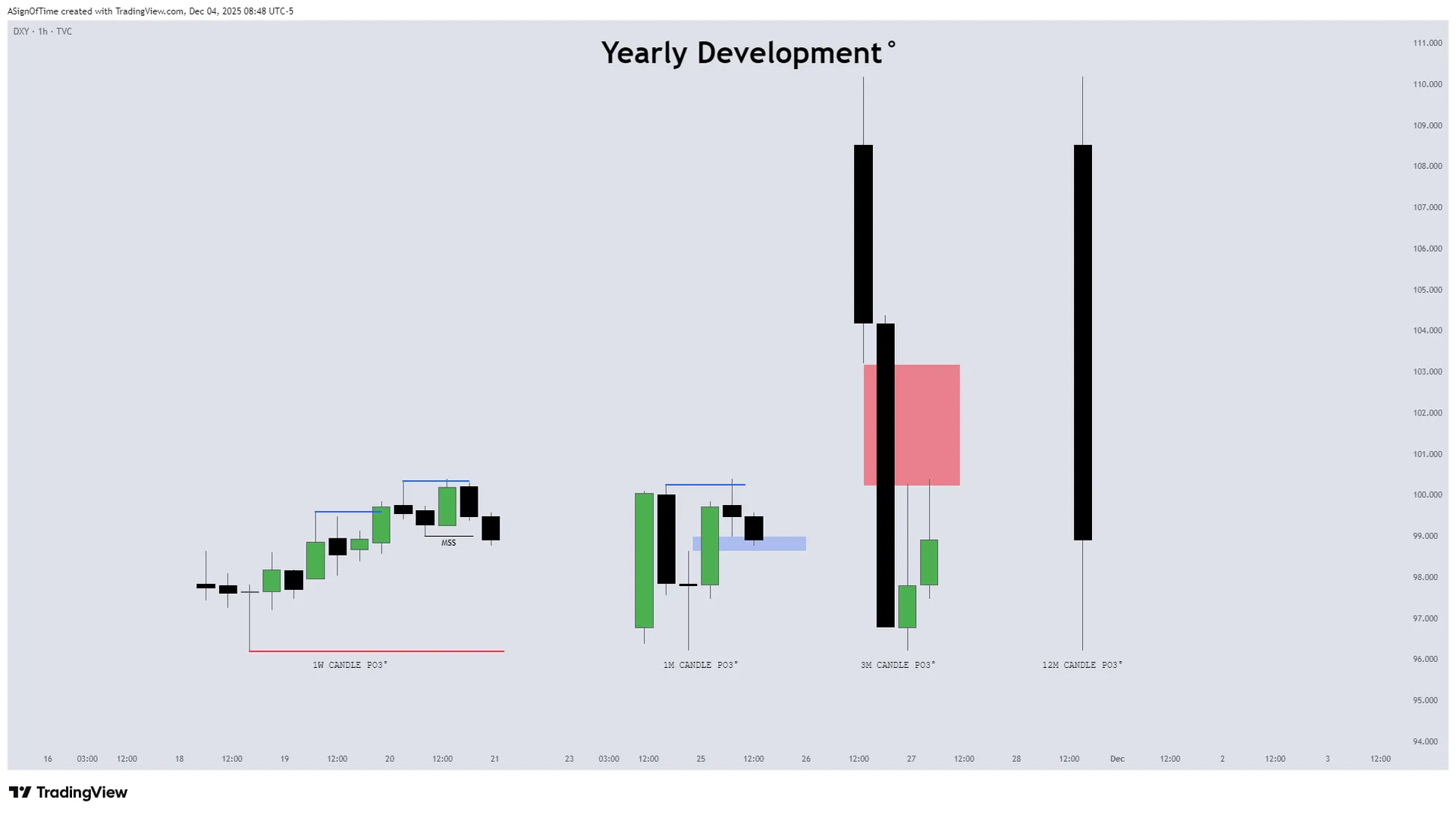

Featured Indicator